Subscribe for the latest updates

Sign up for our newsletter to get the inside scoop on all things remote work and global employment.

.png&w=3840&q=75)

-1.png&w=3840&q=75)

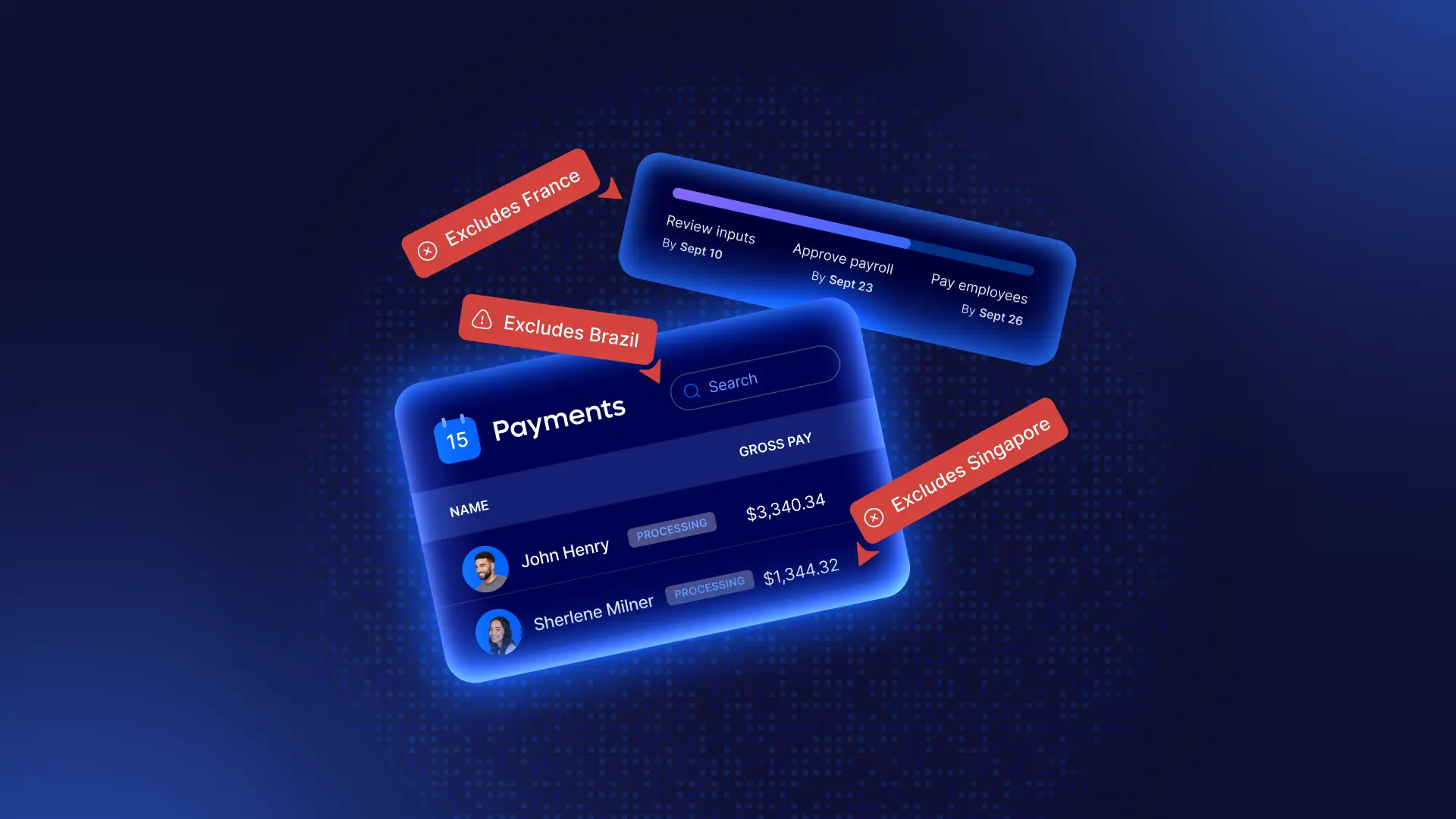

Most global payroll integrations look functional from the outside. These four questions reveal what's actually happening underneath.