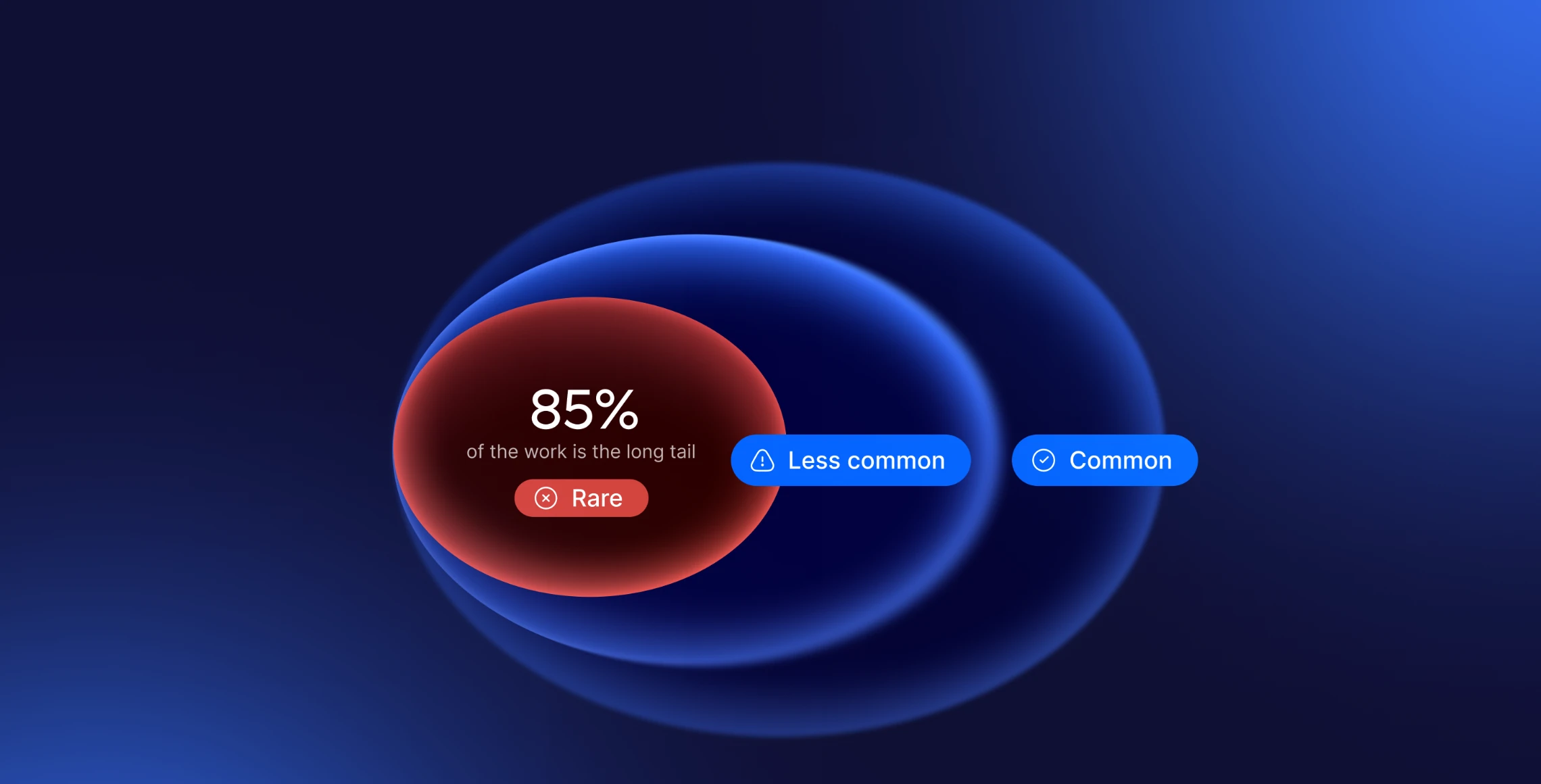

The most complex global payroll market isn't the one you'd guess

Most expansion plans assume payroll cost scales with headcount and statutory rate. Data from 4.8 million payslips says otherwise: operational complexity varies 4× across markets, doesn't track labor cost, and concentrates in places most forecasts overlook — like the Philippines.

Recent stories

.png?width=3840&quality=90&auto=webp&disable=upscale)

-1.png?width=3840&quality=90&auto=webp&disable=upscale)